Define a VAR(1) model as a function handle Github code

This example shows how to define a VAR(1) model as a function handle to work with VBLab supported VB algorithms.

Let ${y_t,\ t=1,2,…}$ be a $m$-dimensional time series. Consider the vector autoregressive model of order 1, denoted as VAR(1), defined as:

\[y_t = c+ Ay_{t-1} + u_t, \quad u_t \sim^{iid} \mathcal{N}(0,\Gamma)\]where $c$ is a $m$-vector and $A$ a $(m\times m)$-matrix of regression coefficients. For the simplicity, let’s assume $\Gamma$ is known. The vector of model parameters is $\theta=(c^\top,\text{vec}(A)^\top)^\top$. Suppose that the prior is $p(\theta) = \mathcal{N}(0,\sigma_0^2I_d)$ with $I_d$ the identity matrix and $d=m(m+1)$.

Then the $h(\theta)$ term of the VAR(1) model can be derived as

\[\begin{eqnarray}\tag{1}\label{eqn:var1-1} h(\theta)&=&\log p(\theta)+\log p(y|\theta)\\ &=&-\frac{d}{2}\log(2\pi)-\frac{d}{2}\log(\sigma_0^2)-\frac{\theta^\top\theta}{2\sigma_0^2}-\frac{m(T-1)}{2}\log(2\pi)-\frac{T-1}{2}\log|\Gamma|\\ &-&\frac{1}{2} \sum_{t=2}^{T} \left((y_t-Ay_{t-1}-c)^\top \Gamma^{-1} (y_t-A y_{t-1}-c)\right). \end{eqnarray}\]and the $\nabla_\theta h(\theta)$ term can be written as

\[\begin{eqnarray}\tag{2}\label{eqn:var1-2} \nabla_\theta h(\theta) = \begin{pmatrix} \nabla_c h(\theta)\\ \nabla_{\text{vec}(A)}h(\theta) \end{pmatrix} \end{eqnarray}\]with

\[\tag{3}\label{eqn:var1-3}\nabla_c h(\theta) = -\frac{1}{\sigma_0^2}c+\Gamma^{-1}\big(\sum_{t=2}^T (y_t-A y_{t-1}-c)\big)\]and

\[\tag{4}\label{eqn:var1-4}\nabla_{\text{vec}(A)}h(\theta) = -\frac{1}{\sigma_0^2}\vec(A)+\sum_{t=2}^T y_{t-1}\otimes \big(\Gamma^{-1} (y_t-A y_{t-1}-c)\big).\]Given the equations to compute the $h(\theta)$ and $\nabla_\theta h(\theta)$, we will define a function, following the template discussed before, to define the VAR(1) model that can work with VBLab supported VB algorithms.

For demonstration, we create a simulation data including $2$ series of $100$ observations, generated from a uniform distribution.

% Setting

m = 2; % Number of time series

T = 100; % Number of observations

% Generate data

y = randn(m,T);

Then, we prepare the additional information needed to compute the $h(\theta)$ and $\nabla_\theta h(\theta)$ terms of the VAR(1) model. This information will be stored in a struct named setting. The additional information include priors, number of model parameters, indexes of model parameters in the vector of variational mean and the covariance matrix $\Gamma$.

% Additional setting

setting.prior.mu = 0;

setting.prior.var = 1;

setting.y.mu = 0;

setting.idx.c = 1:m; % Indexes to extract c from a vector of all parameters

setting.idx.A = m+1:m+m^2; % Indexes to extract A from a vector of all parameters

setting.num_params = m + m^2; % Number of model parameters

setting.Gamma = 0.1*eye(m); % Fixed covariance matrix

Next we prepare initial values for the variantional mean (optional) and run the CGVB algorithm to estimate the model parameters

% Prepare theta

c = rand(m,1);

A = rand(m);

% Initial variational mean

theta = [c;A(:)];

Post_CGVB_VAR = CGVB(@grad_h_theta_VAR1,y,...

'NumParams',setting.num_params,...

'Setting',setting,...

'LearningRate',0.002,... % Learning rate

'NumSample',50,... % Number of samples to estimate gradient of lowerbound

'MaxPatience',20,... % For Early stopping

'MaxIter',5000,... % Maximum number of iterations

'GradWeight1',0.9,... % Momentum 1

'GradWeight2',0.9,... % Momentum 2

'WindowSize',10,... % Smoothing window for lowerbound

'GradientMax',10,... % For gradient clipping

'LBPlot',false);

Finally, we need to define the function grad_h_theta_VAR1 using the template discussed in how to define models as function handles. The grad_h_theta_VAR1 can be defined in a seperate script named grad_h_theta_VAR1 or at the end of the example script.

%% Function to compute the gradient of h(theta) and h(theta). This can be defined in a separate file

% Input:

% y: mxT matrix with M number of time series and T lenght of each time series

% theta: Dx1 array of model parameters

% setting: struct of additional information to compute gradient h(theta)

% Output:

% grad_h_theta: Dx1 array of gradient of h(theta)

% h_theta: h(theta) is scalar

function [grad_h_theta,h_theta] = grad_h_func_VAR1(y,theta,setting)

% Extract size of data

[m,T] = size(y);

% Extract model settings

prior_params = setting.Prior;

d = setting.num_params;

idx = setting.idx;

Gamma = setting.Gamma;

Gamma_inv = Gamma^(-1);

% Extract params from theta

c = theta(idx.c); % c is a Dx1 colum

A = reshape(theta(idx.A),length(c),length(c)); % A is a DxD matrix

% Log prior

log_prior = Normal.logPdfFnc(theta,prior_params);

% Log likelihood

log_llh = 0;

for t=2:T

log_llh = log_llh -0.5*(y(:,t) - A*y(:,t-1)-c)' * Gamma_inv * (y(:,t) - A*y(:,t-1)-c);

end

log_llh = log_llh - 0.5*m*(T-1)*log(2*pi) - 0.5*(T-1)*log(det(Gamma));

% h(theta)

h_theta = log_prior + log_llh;

% Gradient of log prior

grad_log_prior = Normal.GradlogPdfFnc(theta,prior_params);

% Gradient of log likelihood;

grad_llh_c = 0;

grad_llh_A = 0;

for t=2:T

grad_llh_c = grad_llh_c + Gamma_inv*(y(:,t) - A*y(:,t-1)-c);

grad_llh_A = grad_llh_A + kron(y(:,t-1),Gamma_inv*(y(:,t) - A*y(:,t-1)-c));

end

grad_llh = [grad_llh_c;grad_llh_A(:)];

% Gradient h(theta)

grad_h_theta = grad_log_prior + grad_llh;

% Make sure grad_h_theta is a column

grad_h_theta = reshape(grad_h_theta,d,1);

end

We can manually plot the variational distribution together with the lowerbound. The convergence of the lowerbound shows that the CGVB works properly in this example.

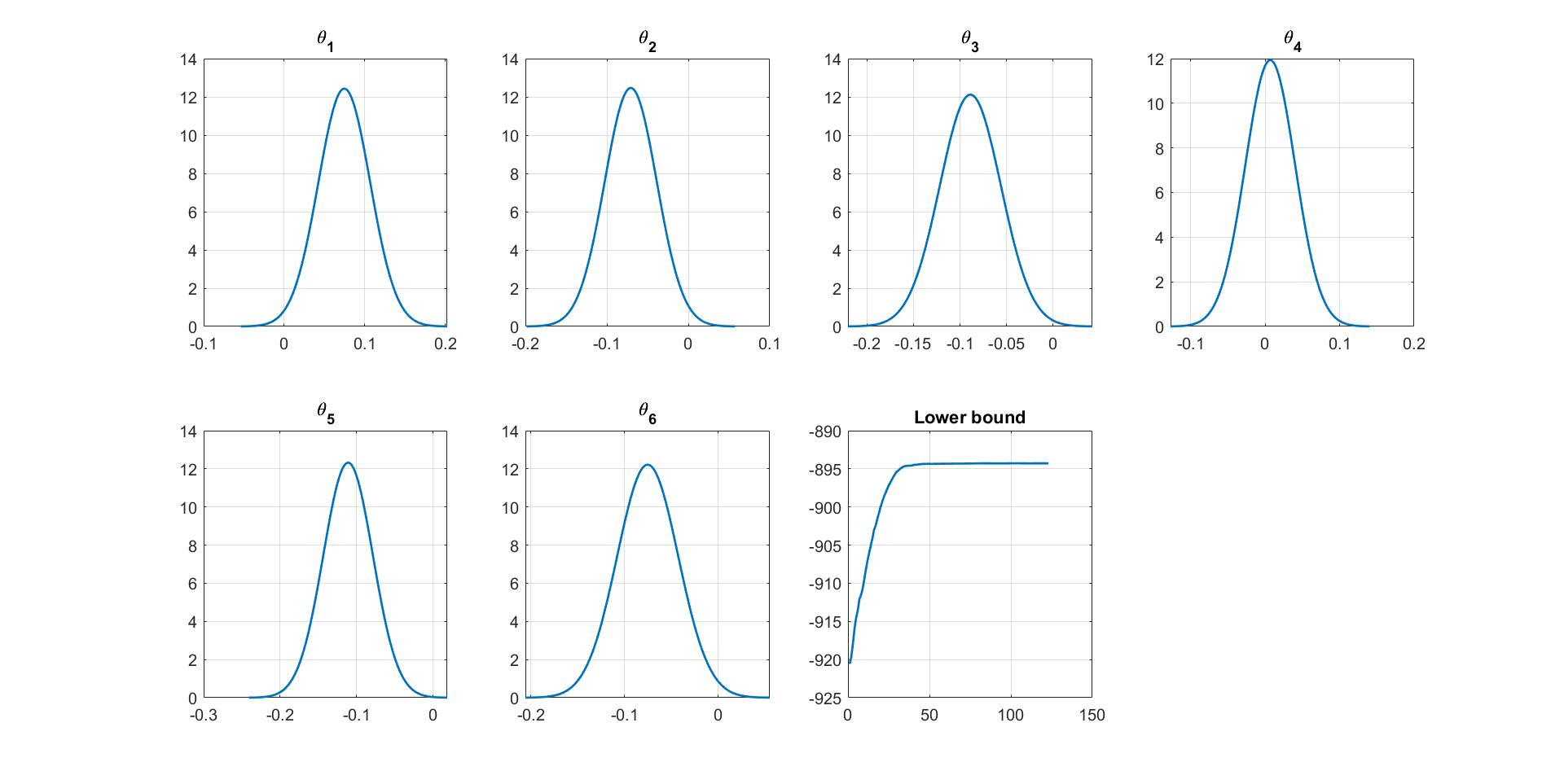

% Plot varitional distribution and of model parameters

figure

% Extract variation mean and variance

mu_vb = Post_CGVB_VAR.Post.mu;

sigma2_vb = Post_CGVB_VAR.Post.sigma2;

% Plot the variational distribution of each parameter

for i=1:mdl.num_params

subplot(2,4,i)

vbayesPlot('Density',...

'Distribution',{'Normal',[mu_vb(i),sigma2_vb(i)]})

grid on

title(['\theta_',num2str(i)])

set(gca,'FontSize',15)

end

% Plot the smoothed lower bound

subplot(2,4,7)

plot(Post_CGVB_VAR.Post.LB_smooth,'LineWidth',2)

grid on

title('Lower bound')

set(gca,'FontSize',15)